What will property prices likely do in a period of UK stagflation?

Some people say that history rhymes. Well certainly studying what has happened in similar situations in the past, does help us to predict and anticipate what may likely happen in the future.

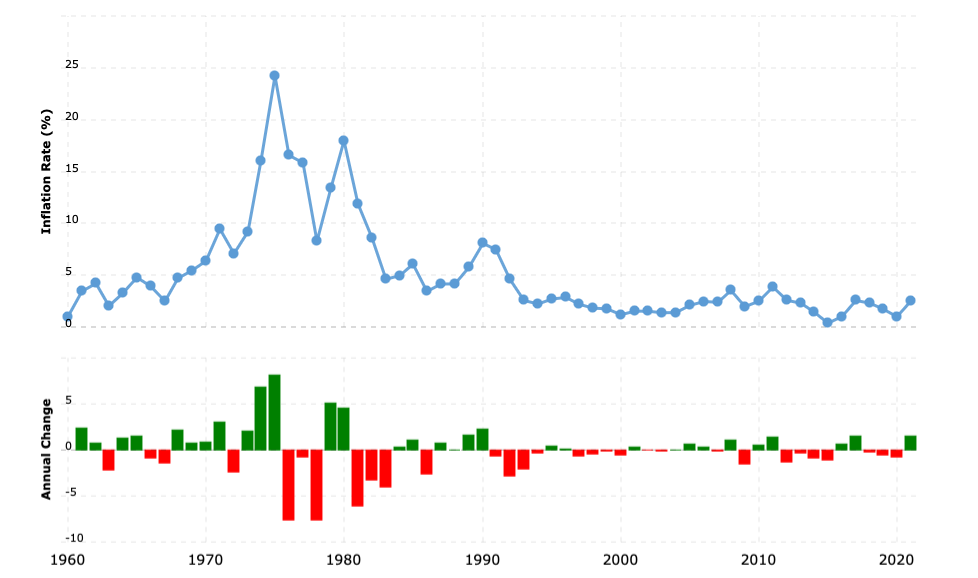

UK Inflation Rates over the last 50 years

(Click graph to view larger)

Right now, the UK is experiencing increased inflation with low growth rates, commonly termed as a period of stagflation. The sense of uncertainty and perceived turmoil, especially when reading the news, may cause many investors to freeze and do nothing instead of studying past situations which are similar to what we are experiencing today, to give a clue or to help them to anticipate the likelihood of various scenarios.

Historically UK Property prices have done well in periods of high inflation with high energy costs and low growth. The last time that the UK was in quite a similar situation as today, with high inflation fuelled by an energy crisis and low growth was in the 1970s, where inflation spiked at 24%. Meanwhile, UK property prices increased during the same period and boomed thereafter long term. Any period of negative house price growth was normally short-lived and sharp, when compared to the long-term trend.

Sources: World Bank via macrotrends.net

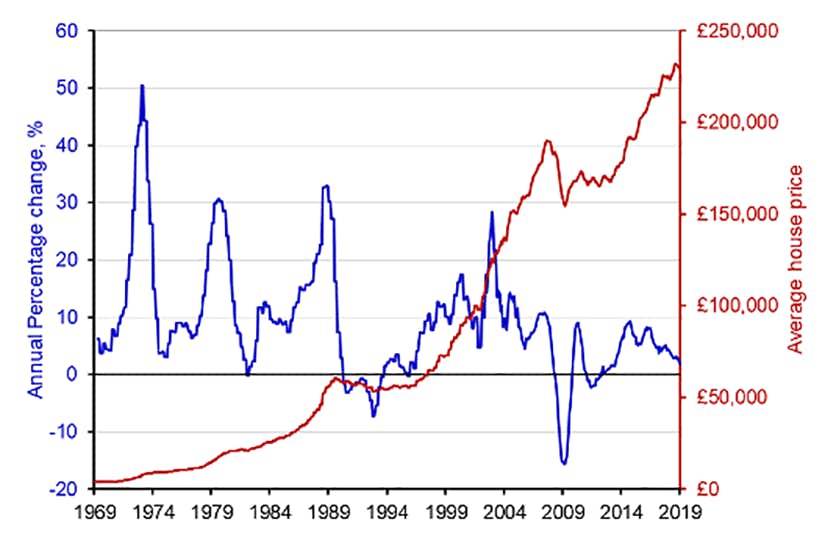

UK House Prices

(Click graph to view larger)

Sources: UK House Price Index: Reports (Office for National Statistics)

A different way of looking at property prices rising, is instead realising that it is more about our basic currencies being devalued through money printing or Quantitative Easing. As Ray Dalio comments in his latest book “The Changing World Order”, “the biggest risk in the long run is the “currency value of money” risk, which most people don’t pay enough attention to… creditors will hold assets that will be devalued”.

This is why holding cash in the bank, to play it safe and do nothing is the greatest risk to long term wealth preservation, especially in times of high inflation. The current UK inflation rate is 11.1% eroding bank balances by this value annually. UK property increased nearly 11% during the last year giving a difference in capital growth of over 20% by holding UK property instead of cash. Investors should enjoy a solid ROCE in addition to any capital appreciation, making the returns on holding property for letting stronger still, subject to the right lettings model and management.

This is one of the reasons that I am so passionate about UK property and helping people to get a long-term stake in property, a real physical durable asset, to help them to prosper and live a life on their terms.